Trying to explain to a client who purchased an unoccupied property insurance from you some time ago that they are not insured for anything but fire, aircraft, explosion and earthquake at the point of a claim is always tricky. Sure, if you have backed up your advice at the time with the right sort of words, then your firm’s PI policy will be in the clear, but if you haven’t it’s likely that a client who perceives that they have no place to go financially may decide to pursue you.

Clients have a habit of taking the cheapest option much of the time but not really understanding, beyond the premium, what the implications of that decision are until it’s too late. Some time ago we decided that we would not sell limited perils insurance for existing structures however badly our clients remonstrated about the premium of an all risks cover. What we found is that the vast majority are willing to pay for all risks if they understand clearly what the differences are between the two policies and why we don’t offer them.

Offering FLEA products focuses the client’s mind away from the cover considerations and firmly on premium. When you take this advice in the context that less than 20% of our claims are fire related, you’ll understand why taking a firmer line at the point of sale is doing you and your client a favour.

New findings from GoCompare have made the papers in recent weeks, with research recently commissioned highlighting that a large number of property owners are not informing their home insurers of the renovation plans.

The research states that 43 per cent of UK homeowners have carried out major work on their property in the last five years, but 41 per cent of those have not informed their insurer of the changes made.

Having not informed their home insurer, it means those who splash out over home improvement works are at risk of invalidating their insurance policy – for renovations such as a new bathroom or kitchen, or installing a new boiler or central heating system. As far as we’re concerned, it’s not a deliberate act to deceive or miscommunicate with their insurer – most property owners just won’t know that they should. And that’s the most worrying thing.

As an expert in placing renovation insurance for high net worth properties across the country, we can’t say we’re surprised. In fact, we think it’s a sign of a clear trend more widely – in terms of the distinct lack of awareness and understanding in this whole area. What is surprising in all this though is that people have no idea of the risks they and their properties are under without the correct insurance in place.

It’s exactly the same scenario in the high net worth property market, where your standard home insurance definitely won’t cover the work. With works undertaken being so vast and costly, if you don’t have specialist renovation insurance, you’re not covered at all.

A big risk, a huge issue – but not widely known.

GoCompare’s findings very much mirror our own experiences here at Renovation Insurance Brokers. We regularly talk to customers about the need for renovation insurance to cover their works; an important part of the process but not an area that’s widely known about. Even when property owners are spending in excess of £500k and up to the millions on their property renovations, insurance doesn’t always get considered.

This has got us thinking – and the true percentage across the whole market may actually be much higher than the GoCompare figures state, when you take into account the large scale renovations market too.

Here’s a list of just some of the risks that will not be covered by your standard buildings insurance include:

Fire or damage to property caused by your contractor’s negligence

Any damage to your neighbour’s property as a result of your renovation works

Instability due to potential structural changes

Theft of valuable building materials on site

Property being exposed to the elements due to an open roof

Burst pipes before the project is complete

Our advice? Before undertaking any form of property renovation, ask the question and have the conversation – whether that be with your existing home insurer for small works, or your architect or project manager for larger ones. Not being insured is not a risk that’s worth taking.

The Grand Designs Live show in London has shut its doors for another year – and once again thousands of individuals descended on London’s ExCel to be inspired and educated for their current or upcoming building project. In our last blog, we wrote about our pride in being invited to be part of the Ask the Expert session taking place during the show. For our latest article, our Managing Partner Douglas Brown offers his insights and perceptions on an event that included his contribution for the first time.

“Our whole business has been built on offering high value renovation advice to those who need it – so to have the opportunity to do this on a larger scale at the highly regarded Grand Designs event was truly wonderful. The event was incredibly well organised and full of innovative manufacturers and designers; all beautifully presenting their products and approaches for builds and renovation projects of the future.

The exhibition halls were packed – but the Ask the Expert panel area, less so. The opportunity to speak directly to experts from across the spectrum was hugely underutilised. That was surprising in itself – but even more so was the fact that only individuals who had suffered a serious loss were even thinking about the insurance angle.

Individuals that have experienced an insurance problem, now have their eyes wide open to the risks and vulnerabilities – and rightly wanted to protect themselves this time. But what about for those who didn’t come and see us? Like so many other renovators across the county, with their future renovation, they are sleepwalking into risk.

We provided our expertise over three days of the show, and had good conversations with over 20 people. I heard first hand from a couple that had lost everything in a fire to their renovated property that wasn’t covered – and are now having to work tirelessly to rebuild it with no insurance pay-out. They were keen to tell me their story to tell me of the damage that it had done both literally and emotionally, and to tell me they wish they’d understood what was needed to be fully protected.

Thanks for having us Grand Designs Live. We had some very good discussions – but it was clear from speaking to current and future renovators face to face that there is a huge lack of awareness on the insurance requirements and technicalities during a renovation. I was pleased to be able to educate the few on the day, but for the many – our work goes on. I can’t reiterate enough the risks there are to your renovation without the proper insurance in place.” – Douglas Brown, May 2017

You don’t need to wait until the next Grand Designs show to ask our experts about your renovation project and its likely insurance requirements. Give us a call on 08442 641200 to speak to one of our team about your plans – we’d be happy to advise you.

Renovation is booming, particularly at this time of year. If it’s on your agenda, don’t let your home upgrade leave you financially exposed. That is the advice from our managing partner Douglas Brown, the founder of Renovation Insurance Brokers, and the figurehead at the forefront of a new initiative to make sure home owners are appraised of the facts.

If you are thinking of spending £100,000 or more on an upgrade to your home it is essential to make sure you have specialist insurance cover. Douglas was recently invited to speak on this very topic as one of the ‘Expert Panel’ to visitors of the 2017 Grand Designs London Live at ExCel, an event based on the hugely successful Channel 4 TV series presented by Kevin McCloud.

As experts in building contract compliant insurance, we work to ensure a property is protected during the renovation process. One of the key issues encountered is that the home owner often doesn’t understand what insurance is needed because it’s not just house insurance.

Unfortunately, it is often only in the event of a problem that the lack of insurance is brought to life; when it’s so desperately needed but not in place. Douglas tells us more: “A recent example we heard of was a new water hydrant blowing in the basement of a new renovation. The home owners discovered that their insurance only covered fire or lightening, when what they really needed was an all-cover risks for works and buildings. It’s a very costly mistake to make.”

With the high costs and inconvenience involved in moving, it’s no surprise that many people are deciding to renovate their homes instead. Basement developments and loft extensions are increasingly popular renovations, especially in sought-after postcodes.

However, there is very limited public awareness that standard building insurance is not likely to cover any renovation costing £100,000 or more. That is why having project building contracts properly insured is critical, because of the potential pitfalls of unforeseen renovation problems being hugely costly if it is not in place.

Renovation Insurance Brokers solves the problems of adverse risk and unpredictability by providing home owners with specialist insurance. We cannot reiterate strongly enough how important it is to ask the right questions of your advisors regarding insurance, before embarking on their renovation plans. If you’ve got any questions for us, we’re ready to answer them. Get in touch.

Here’s a question for you – who’s advising you on your renovation project? If you are planning on undertaking a large scale renovation in 2017 or have a large project underway, you’ll need good advisers around you.

The project team that you are working with are likely to have experienced renovations like yours before and you are likely to have chosen them due to that clear expertise. But for you, it’s perhaps your first time – and in fact, possibly the only time that you’ll be living and breathing the renovation process. You’ll learn a lot as you go along, and lots of that learning will come from those who are working on the project with you. Ask their advice, listen to their suggestions, do your own research and if needed, get a second opinion.

In a blog last year, we talked last year about the importance of advice in the planning of renovation. We’re delighted that our plea has been heard, with our Managing Partner Douglas Brown invited to participate in a popular Ask the Expert session at this year’s Grand Designs Live.

Based on the hugely successful Channel 4 TV series, Grand Designs Live runs from Saturday 29th to Sunday 7th May at Excel in London. In the Ask the Expert area, Douglas is one of just a few handpicked professionals invited to be part of the event; to offer support, advice and reassurance to some of the thousands of visitors due to come through the doors during the exhibition.

In adding renovation insurance to the already popular Ask the Expert sessions, Grand Designs Live is demonstrating to its visitors how important advice really is in the renovation process. In our business, we know first-hand how important it is to get renovation insurance agreed before a renovation project begins – but most renovators do not. To have the opportunity to advise them in this area is something we are hugely excited about. We’ll share more in a wrap up report after this year’s event!

We know not everyone will be able to make it to Grand Designs Live – so don’t forget that we are on hand at any time to talk about your renovation insurance enquiries. If you’ve got a renovation insurance request or enquiry right now, you can get in touch with our expert team here.

It’s important to understand why customers buy insurance and why they choose a broker to buy it from.

The former is pretty clear for two reasons:

The subject of the insurance is something they cannot afford to lose.

They don’t know what’s going to happen in the immediate future.

So we solve the problems of adverse risk and unpredictability by providing them with insurance, in this instance for their home undergoing renovation. But why do they choose a broker to buy it from? On the face of it everyone seems to have forgotten the answer to this question and it has nothing to do with price.

The customer doesn’t understand what insurance is needed because it’s not just house insurance.

The customer doesn’t know where to get this type of insurance.

Nobody in a call centre understands it either.

So the client comes to you, usually late on in the pre-project period and makes an enquiry for JCT compliant insurance what should you do? Are there any steps you can take to make the sales process smoother and less painful for you both? Yes there are.

Try the following:

Be direct and say that the insurance required is non-standard and only provided by a few underwriters, because most insurers decline.

Make it clear that the reason for this is because of the claims record of property undergoing works. Very large infrequent losses which are difficult to predict.

Insurance companies like predictability in risk and this just doesn’t fit with their appetite.

Reassure them that you will be able to arrange something in time.

Use the quick quote calculator to provide an range of premium.

If they are unpleasantly surprised make it clear that their home is becoming a building site and doesn’t represent a home any more.

Say that the cost will be offset against the buildings insurance they would have had to pay, it’s not in addition to it.

The cover includes their works and property owner’s liability which is important when riskier things are happening on the site.

The JCT places an obligation upon them to insure and it’s better to stay in control of their largest single asset.

The product that you are proposing to them is the closest thing to a good quality HNW home insurance.

These simple tactics give you time to win them over and help them understand what the implications of insuring badly are. They also give you the opportunity to show your expertise and prove your worth to them.

At that point you are a respected and trusted advisor who can help them solve a very specific problem, you are providing value for money, which is what professional brokers do!

It’s important when the client’s contractor is joint insured that they understand the terms under which they and their sub-contractors are operating. The intention of our policy is to insure the works and the structure from top to bottom, particularly when a JCT joint names contract is in place.

The problem arises when a client does not cascade the terms of the insurance to the contractors who are working for them, yet expects them to be bound by the policy terms and conditions. This makes subrogation harder if a negligent act breaches a policy condition and, in the longer term, leads to higher rates for all.

Given that the intention of the wording is to insure the contract, whosoever undertakes the work (contractor or sub-contractor), it’s important that other contractual arrangements don’t get in the way. As an example, if a main contractor’s terms and conditions specify that any sub-contractors are responsible for materials and their work until the end of the contract, it’s possible it could obstruct a payment being made on the basis that the client was not contractually obliged to insure the works; not great. Your client is not going to be happy if his own insurers tell him he has no cover, and that he should pursue the sub-contractor’s own works policy.

To cut this situation off we recommend that your clients advise their contractor of the insurance placed by them and send them a copy of the policy schedule and wording. At the same time they should make it clear that the intention of the policy is to insure all works under the contract and that any terms stating otherwise between the main contractor to sub-contractors should be withdrawn.

We’ll be issuing guidance notes for main contractors very shortly to go out with all policies and would like you to help us make sure these filter down to contractors and their sub-contractors by pointing this situation out to your clients.

Whilst this introduces another layer of complexity to the arrangements, it does make sure that the lines of liability are clear such that claims can be settled quickly and fairly, whilst leaving the door open for subrogation if required.

In our upcoming policy review we’ll be looking to firm up this area by making it clear within the wording that regardless of the terms under which sub-contractors are operating, ours is the primary insurance and will react if an insured event occurs.

Our Renovation Insurance Specialist, Matthew Dover discusses Brokers attitudes towards securing brokerage, and how it’s important to educate clients as to why the cheapest price, doesn’t necessarily mean the best value for money.

“The bitterness of poor quality remains long after the sweetness of low price is forgotten” – Benjamin Franklin

In all my years of broking, primarily around property renovations within the high-net-worth and mid-net-worth sector, I often wonder where the line between price and advice falls.

It’s sometimes the case that Brokers are dumbing down their advice and providing inferior products to reduce costs to their clients and secure brokerage. In the end, who loses out more, the Broker or the client? In reality, what’s bad for one is generally bad for the other.

In my opinion, it’s in our best interests, as well as our core responsibility as Brokers, to advise clients honestly on the right cover price mix, with price a secondary consideration. Our experience tells us that peace of mind does trump low premiums when clients are truly aware of what they are buying. In the direct channel we convert 84% of our opportunities which tells us that when you know what you are talking about the chances are you will provide the right policy.

Sometimes, you’re better off walking away from a customer who isn’t prepared to insure properly, than offer a cheap solution that isn’t going to work if there’s a claim. Remember works claims are complicated enough without having to worry about what’s covered!

Whilst it may be the case that some clients are just looking for cheap premiums, I wonder whether the conversations Brokers are having with clients are happening in the right way. The customer will initially focus heavily on price, but, I believe that we should try and liberate them from this mind-set and instead, talk about value for money.

Low price isn’t necessarily always the right price and it’s up to us as Brokers to explain to our clients why this is the case. If our clients can make an informed decision, then more often than not they’ll make the right one.

And for those who don’t make the right decision, ask them what they value more – the peace of mind knowing they have the best cover on the market, or inadequate cover that leaves them exposed should things go wrong? If they still don’t bite, perhaps it’s time to walk away or at the very least make sure they know what they are NOT covered for.

As a general rule of thumb, price is less of an issue the higher up the client net worth spectrum you go, with mid-net-worth clients often being the ones looking for unrealistic renovation insurance premiums based on their knowledge of household insurance. However, it’s often the case that the mid-net-worth clients of today are the high-net-worth clients of tomorrow, therefore it’s worth going through the pain of educating them early on as to why buying cheap doesn’t necessarily mean they will be getting a good deal.

I’ll be ever so slightly biased in recommending our Broker CPD training, but for those of you who haven’t already, signing up to this year’s Renovation Insurance CPD programme, commencing 14th February, won’t be the worst thing you have ever done.

It picks up on the issues raised above, as well as provides you with the knowledge of renovation insurance in private client and commercial divisions required to provide the best advice for your clients.

I’m willing to bet that after spending two hours with us, your insurance knowledge will be expanded and you’ll be thinking more like an insurance professional and less about racing to the bottom on premium. As a bonus you can register two hours of structured CPD for your records.

If this is the year you’ll be undertaking a large scale renovation, you won’t be alone. Already this year, the news and property pages are forecasting an extremely positive year for the UK property market on the back of solid growth reports in the final months of 2016 from manufacturing and construction firms. As is often the case, we once again expect a large number large scale renovation projects to be undertaken across the country too.

Now, we know that insurance isn’t going to be the first thing on your renovation ‘to do’ list – but it’s hugely important to understand your insurance requirements and obligations so that your project is fully planned and protected from the start.

Here’s a rundown of just some of the key considerations you’ll need to make before undertaking a 2017 renovation project.

How’s it looking? Assess the property structure before you start.

You’ll hear the term ‘existing structure’ – in essence the walls and boundaries that exist in the property you are renovating. Make sure you’re clear on the type/s of construction and any listing on the building and get a fair assessment of the building condition. You’ll also need to understand rebuild cost and be ready to disclose any unusual features or enhanced risks (for example, a history of subsidence or flooding) before you start. The insurance premium you pay and extent of cover you’re able to obtain will be dependent on all these factors. Find out more.

What’s it going to cost? Prepare a complete calculation.

As renovation insurance experts, we can help you calculate the correct sum so that your works are correctly insured. You’ll need to estimate the total project duration from inception to practical completion, and have a broad understanding of the risks you’re going to face, particularly enhanced risks, so that the premium you’re quoted can be viewed entirely in context. We share more here.

A large scale renovation project is a big deal. What’s your liability?

It’s common knowledge that building sites can be dangerous places, and, as the employer and property owner, you’ll need to understand who is responsible for what. The extent of your direct liability for third party injury or property damage will depend on the set-up and management arrangements for the project. We tell all here.

Heard of The Party Wall Act (1996)? It might apply to your project.

Whilst The Party Wall Act may not be familiar to you, it will impose obligations and liabilities upon you in certain circumstances. Find out if the Party Wall Act applies to you here.

What about structural warranty – will you need it?

If you’re undertaking a new build, or you are substantially extending your property, we’d recommend a structural warranty insurance to cover defective workmanship and structural issues in the future. The applicability of such cover is outlined here.

Will contents be left at the property? Make sure they’re covered.

In high value renovation situations, the scale of work undertaken usually means renovators/property owners live elsewhere for the duration. Contents do sometimes stay on site though, and will need to be protected. Here’s how.

Is the property unoccupied before work starts? You’ll still need cover.

If you’re purchasing a property for development, or moving out well in advance of the start of works, the current insurer is not likely to want to provide ongoing cover. Standard property insurers are generally not interested in insuring unoccupied property. We can arrange this cover for you in advance of the project start date. Find out more here:

Familiar with JCT Contracts? It’s likely you’ll need one.

A JCT Contract is a standardised, and well understood ‘off the shelf’ contract used within the construction industry to set out the responsibilities and obligations of all parties involved in your project, particularly you and your contractor. It is always our advice to utilise this contract, though we don’t insist on it. You can find out more about JCT contracts here:

There you have it – eight essential renovation considerations to fully protect your project, your property, your pride and joy. Our underwriters will take you through all of this when you call up. We’ll ensure you understand what you need and why you need it. They’ll also be available to provide ongoing advice and support as your project progresses.

Renovation Insurance brokers is proud to place insurance for hundreds of large scale renovation project each year – directly working with renovators or in partnership with our qualified network of private client brokers, project managers and architects across the country. Get in touch with us to talk through your 2017 renovation plans.

With 2016 coming to an end, we’ve started to reflect on the year we’ve had and the work we’ve done here at Renovation Insurance Brokers. We share some of the highlights with you here, in our last blog of the year.

We do hope that it’s been a good year for you and that’s where our year in review message starts.

Thank you for being part of the Renovation Insurance team

And we really do think of us all as a team. We’re proud to have grown and maintained excellent relationships across the high net worth and Private Client Broker network. Each of the Brokers we work with plays a part in our business. Together, this year we’ve insured hundreds of large scale property renovations up and down the country…and that’s thanks to you. Together, we are a winning partnership, bound by our desire to professionally and effectively support your clients with their renovation projects.

They say time flies, and it certainly has here. The 12 months we have experienced have once again seen us undertake a number of activities, leading to achievements that we are very proud of, including:

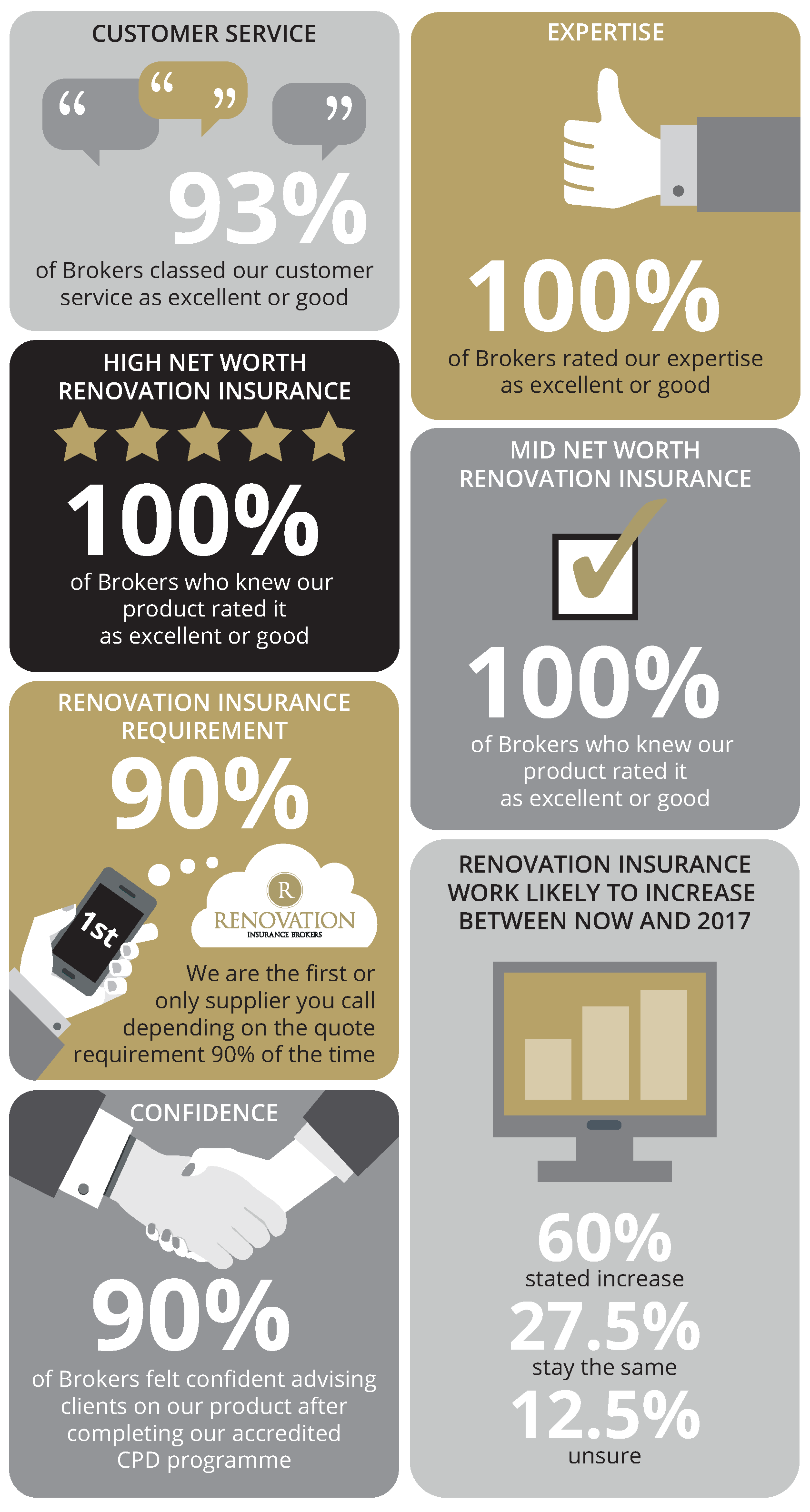

Assessing our approach. We like to think that we are doing a good job – we are passionate about our work and continually drive to offer the very best solutions with exceptional customer service too. This year, we directly asked Brokers what they really thought, with the first Renovation Insurance Brokers Annual Survey. We have to say that we were truly thrilled with the response, with 100% of Brokers rating our expertise as excellent or good, underlining the value we offer through our advice-led approach. We share more of our survey results in this end of year review piece.

Dedicated CPD Training. We launched a brand new Renovation Insurance CPD training programme for Brokers at the beginning of the year, which proved very popular. The initial training dates sold out for January in under a week when advertised in December last year – and the number of dates more than doubled for the period to June 16 due to unprecedented demand. This not only displayed the demand for information on this topic, but also underlines the continuing commitment Private Client teams have in managing client expectations. Results of our Annual Survey showed us that 90% of Brokers felt confident in advising clients on our products, so the training is having the effect that we hoped it would. The demand for our training has been truly phenomenal, so it won’t be a surprise to hear that we’ll be running a new series from the beginning of next year. We’re investing in making our training an even more engaging and rewarding experience too. Register your interest for 2017 CPD Training here.

Strong product portfolio. We’ve worked hard to develop a suite of insurance products that meet the needs of the market. This year’s survey confirmed a 100% excellent or good rating in regards to our products too, which are unlike no others in that they give clients an all risks, peace of mind option at an extremely competitive price. We’ll be undertaking a product review in early 2017 to continue to move us clear of our competition and give clients market leading cover in 2017.

Broker Portal. Our unique portal is well established in the Broker market after being launched nearly two years ago. The majority of our Brokers now have login details for the system, which enables them to obtain a renovation insurance premium indication for their clients more quickly than ever before. Find out about the benefits of using the Broker Portal here.

Clear renovation expertise. Since the very beginning, each year has seen us place insurance for an array of high value, unique renovations in all corners of the country, and this year has been no different. This year we’ve not only seen an increase in the number and size of projects, but also the complexity of both contracts and party wall agreements. It’s a real mix – but each of the renovators and properties we have worked with have all been in need of an expert approach to their challenging insurance requirements. What is evident is that the need for clear and effective advice is at an all-time high, so it’s worth gearing up to make sure you are able to cope.

An expert insurance team. Our long established team has continued to deliver on our vision this year, led by our Managing Partner Douglas Brown. Our senior underwriter Matthew Dover heads up underwriting in Cambridgeshire, while underwriter Chris Harris moved to our London office in Bury Street. We continue to invest in our marketing too, with Marketing Executive Naweed Darr rolling out consistent Broker communications.

Looking forward

We expect 2017 is going to be another intensely competitive year for us all and we hope to be part of your plans for that. A big and wholehearted thank you to everyone who has been part of Renovation Insurance Brokers success this year, we hope that your Christmas is restful and fun.